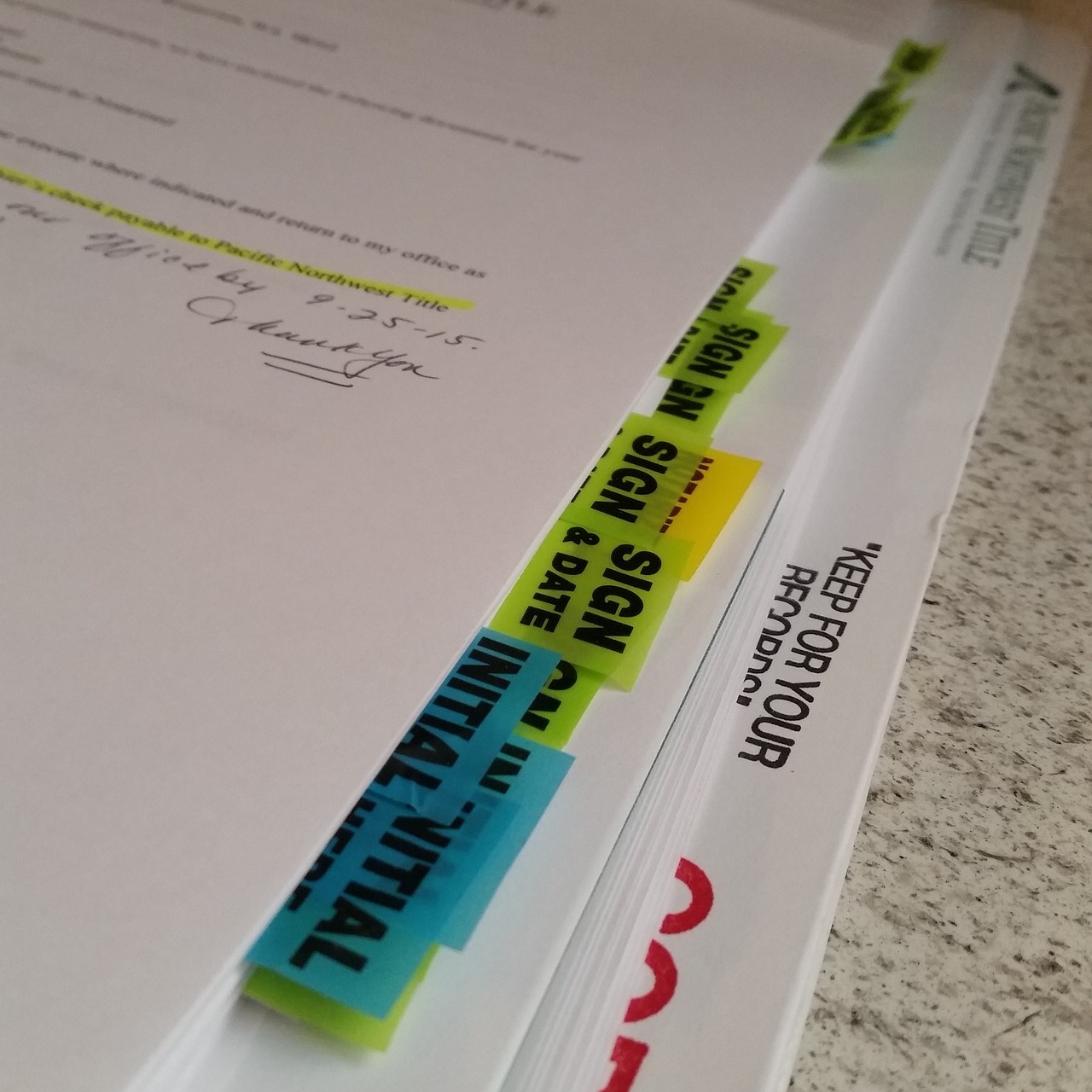

What do I get at closing?

For most real estate loans, you will receive a HUD-1 (if it is a cash transaction) also known as a settlement statement …

or, if you are borrowing money, a Closing Disclosure will be provided to you at least 3 business days before loan consummation – Consumation of closing includes signing and funding the purchase, which frequently happens at the closing meeting.

At the meeting itself you should also receive:

1.) a copy of your Mortgage Note – your obligation to repay-

2.) your Mortgage or Deed of Trust

3.) copies of other documents signed by you, and by the other party, as is appropriate

4.) and you will get the keys to your new home.

What Do I Get At Closing?

You asked, “What do I get at closing?” … but the real question is “what will you not get at closing if you use another title company which does not have the reputation for integrity and professionalism that we do?”

Will you get a caring, friendly, and thorough closing experience which explains every step in your transactions? will you get value pricing, and professional title agents, attorneys, and closers with years of experience?

Indeed, when it comes to choosing a title company in Naples, Florida, for over four decades, real estate professionals recommend First Title & Abstract, Inc.

Let us show you why our commitment to putting you FIRST makes all the difference when you close on real estate.